{kind=link}

There was a time when a big portion of People belonged to the “center class.” It meant you might afford a good dwelling normal, reminiscent of proudly owning a home and a automotive and had financial savings within the financial institution. When “child boomers” reminisce in regards to the “good ole days,” they’re referring to when being middle-class was regular.

Nonetheless, the American center class has continued to contract over the previous 5 a long time. In line with Pew Analysis, the share of adults who reside in middle-class households fell from 61% in 1971 to 50% in 2021.

The shrinking of the center class is accompanied by a rise within the share of adults within the upper-income tier which elevated from 14% in 1971 to 21% in 2021. On the similar time, there was a rise within the share who’re within the lower-income tier, from 25% to 29%. These adjustments have occurred steadily, because the share of adults within the center class decreased in every decade from 1971 to 2011, however then held regular by means of 2021.

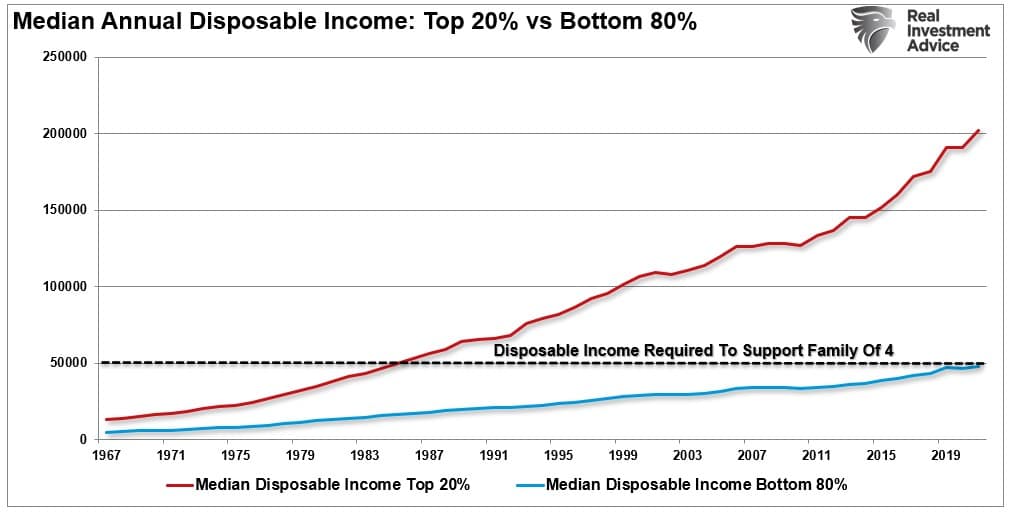

The Census Bureau clearly reveals the issue within the “imply family earnings knowledge” by means of 2021.

{kind=link}

That dotted black line is an important. As with the PEW Analysis knowledge taking a look at incomes alone obfuscates an important a part of earnings evaluation. The query is how a lot earnings it takes to keep up a “middle-class” life-style. Or fairly, what does it take to purchase a home and a automotive and feed two children?

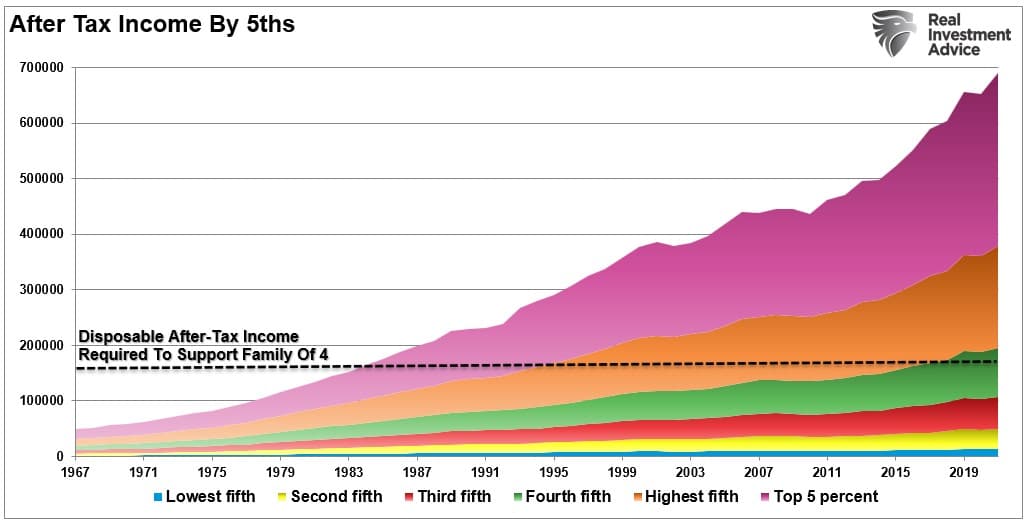

Most significantly, and what’s typically not included within the evaluation, is the usual of dwelling will get “paid for” on an “after-tax” foundation. After we embrace taxation, it turns into clear that roughly 80% of America is failing to assist the “middle-class” life-style.

{kind=link}

As we mentioned just lately, Harvard Enterprise Assessment famous::

“Moreover a booming labor market, exceptionally sturdy family stability sheets assist preserve spending excessive. Households’ internet value is way increased than pre-Covid for each single earnings quintile, offering some buffer to the headwinds of inflation and dour client sentiment.” – Harvard Enterprise Assessment

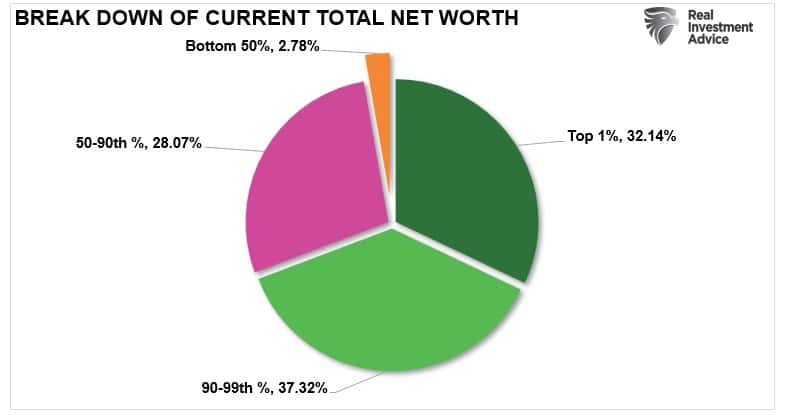

Once more, it’s a true assertion that family internet value has elevated because the Covid lockdown lows. Nonetheless, family internet value is predominately held by the highest 10% of earnings earners, leaving the underside 90% combating over the remaining 30% of the wealth.

{kind=link}

Debt shouldn’t be a alternative for many “middle-class” People.

Extra Debt Isn’t A Alternative

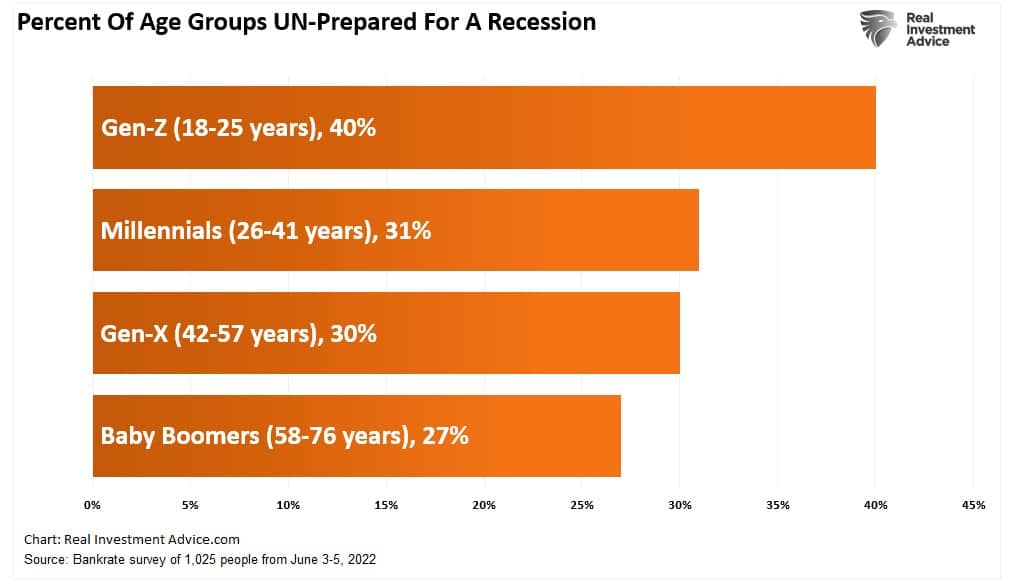

I just lately mentioned “Recession Fatigue” that’s plaguing extra people, in keeping with a BankRate.com survey. To wit:

“When damaged down by era, youthful adults, or Gen Zers, usually tend to expertise ‘recession fatigue’ than millennials, Gen Xers, and child boomers. Within the report, ‘recession fatigue’ is primarily afflicting youthful generations, leaving them unprepared to face a recession. Such knowledge actually flies within the face of media reviews of households having ‘sturdy monetary stability sheets.’”

With the Federal Reserve centered on combatting inflation by tightening financial coverage, the monetary pressures on households will proceed to extend. Given the already excessive ranges of “unpreparedness” for a recession, such leaves a majority of households depending on extra debt to make ends meet.

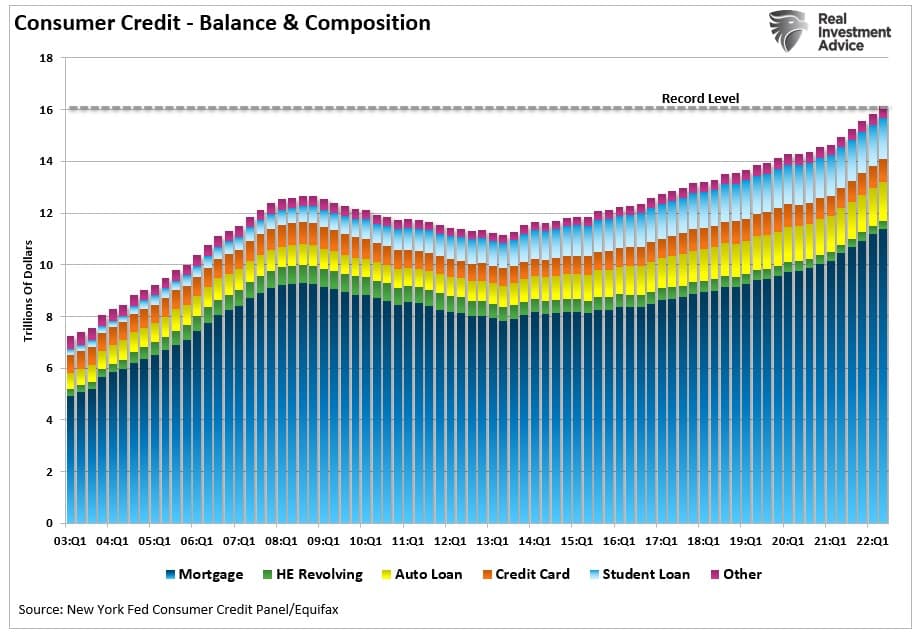

“In line with the newest New York Federal Reserve report, bank card debt surged by $46 billion within the second quarter. As proven above, such isn’t a surprise as shoppers struggled to keep up their way of life. The 13% annualized enhance in new debt was the most important in additional than 20 years. Furthermore, combination limits on playing cards marked their most vital enhance within the final decade.”

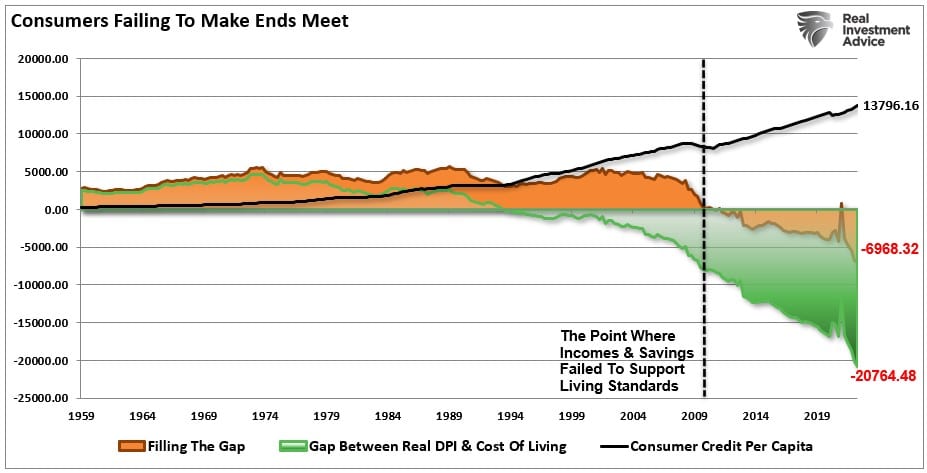

With the pandemic-driven financial savings now spent, 60% of People say they’re dwelling paycheck-to-paycheck. Whereas shoppers can complement their disposable incomes with debt to offset rising inflationary pressures, it’s not a long-term answer. The chart beneath, which requires a short clarification, reveals the issue clearly.

Between 1959 and 1990, people may maintain their inflation-adjusted way of life with solely incomes and financial savings. There was roughly a $4700 surplus yearly as households had very low debt ranges. Nonetheless, starting in 1990 and accelerating following the Monetary Disaster in 2008, it requires an growing degree of debt to “fill the hole” between what earnings and financial savings can afford and the price of the present dwelling normal. You’ll discover a short spike in 2020-2021 as “stimmy checks” hit family financial institution accounts. Nonetheless, that surplus has reversed to the deepest deficit on document.

{kind=link}

Because the “wealth hole” continues to widen between these within the prime 10% of earnings earners and everybody else, the flexibility to keep up a “middle-class” life-style turns into more difficult.

The Highway To Serfdom

In a latest U.S. Information article, many forces form a person’s financial class and their views of the place they rank.

“When requested how they determine their social class, 73% of People mentioned they belonged to the center or working courses, in keeping with an April 2022 survey from Gallup. Fourteen % recognized themselves as an upper-middle class and a pair of% categorized themselves as higher class. In figuring out their social class, folks typically don’t simply take into consideration earnings, specialists say, however different components, together with schooling, location, and household historical past.”

Nonetheless, statistics counsel that if 89% of surveyed people determine as center to upper-class, that solely leaves 11% of the inhabitants on the different finish. Nonetheless, earnings, debt, and internet value statistics clearly present such shouldn’t be the case.

The truth is that middle-class America continues to shrink because the rich-get-richer and the poor-get-poorer. The wealthy can make investments, save and use little or no debt to maintain their dwelling normal, whereas the poor depend on debt, making long-term prosperity an unimaginable purpose.

Moreover, because the peasants demand “extra free stuff” from the Authorities, such requires extra debt and better taxes. These calls for then divert extra capital away from productive funding resulting in slower financial development. As development slows, companies shift to the bottom labor prices, or automation, to decrease earnings development for home employees. Such results in extra calls for from “free stuff” from the Authorities, and the cycle intensifies, pushing extra of the center class downward.

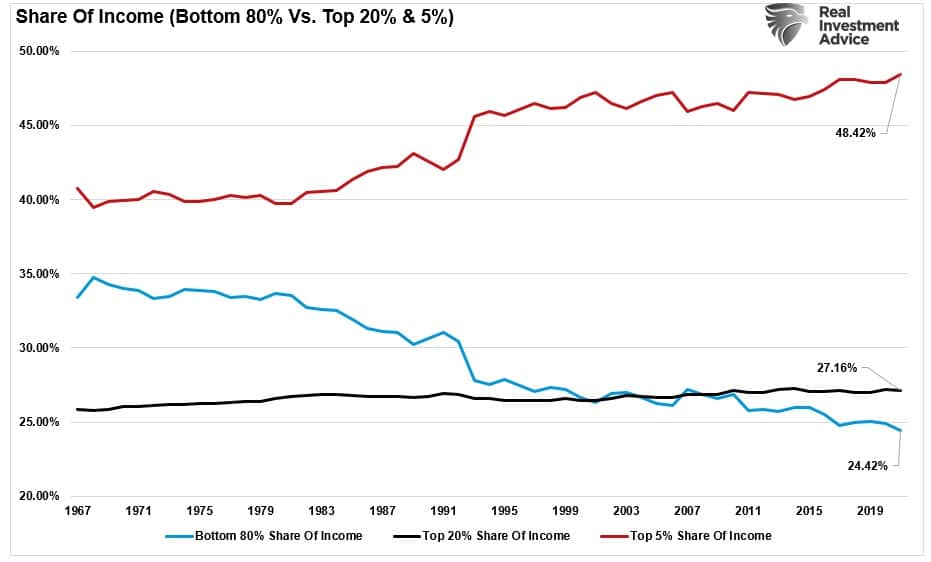

The share of annual incomes between the underside 80% and the highest 5% is proof of that wealth switch from the center class.

{kind=link}

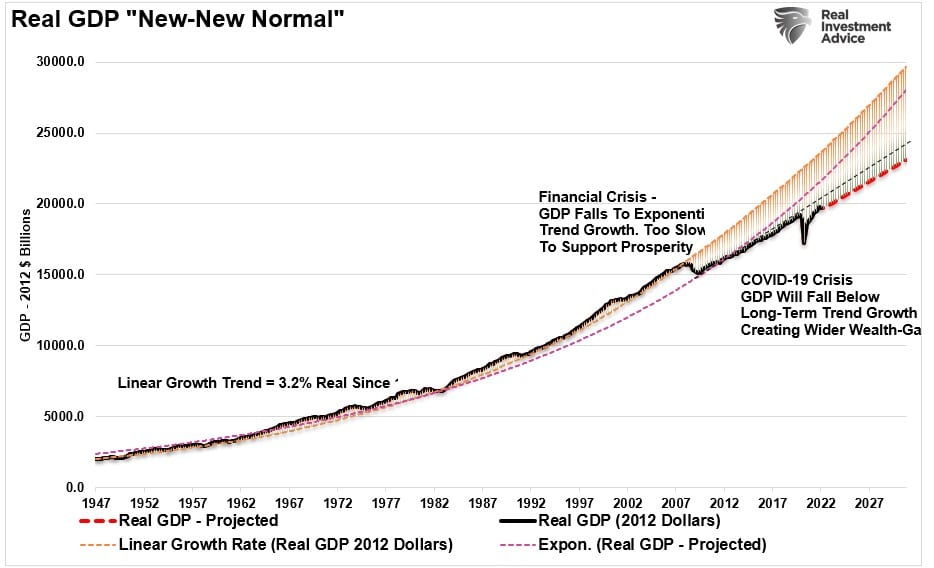

The highway to serfdom is paved with good intentions. After a long time of piling on growing debt ranges to generate financial development, the injury to financial development is changing into extra seen. As proven, financial development tendencies are already falling in need of each earlier long-term development tendencies.

{kind=link}

The tip recreation of an excessive amount of debt, mixed with an ageing demographic, is the “deflationary catastrophe” obvious in Japan’s financial system.

In fact, Japan doesn’t have a center class any longer, both.