.jpeg#keepProtocol)

.jpeg#keepProtocol&description=are+worth+promotions+the+reply+as+a+lean+%E2%80%98golden+quarter%E2%80%99+looms%3F){kind=link}

Web gross sales within the first half of the yr present that, whereas development is down in each quantity and worth on the bumper years of 2020 and 2021, it stays above pre-pandemic ranges. Nevertheless, as family payments soar, shoppers’ conduct is polarizing – elevating the spectre of a lean ‘golden quarter’ for on-line retail in 2022 – except manufacturers can reply with on-point presents.

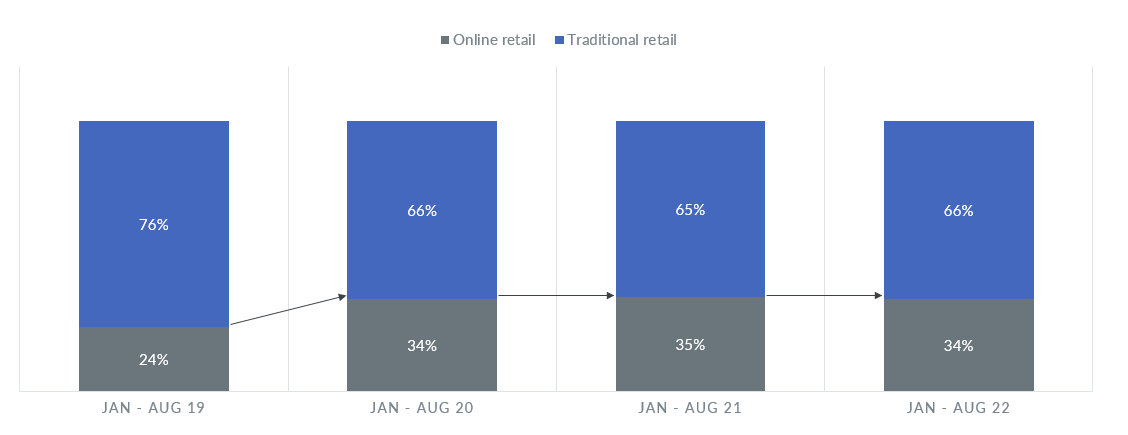

This yr, the share of web gross sales throughout all technical client items’ (TCG) classes globally have continued effectively above pre-pandemic ranges. Conventional retail continues to carry onto a transparent majority, however the indent attributable to expanded on-line procuring habits realized by shoppers and embraced by manufacturers and retailers throughout lockdowns, have remained.

On-line due to this fact continued to account for over a 3rd of all TCG purchases (by worth) made in January to August – degree with the identical intervals in 2021 and 2020, and a rise of 10 proportion factors in comparison with 2019.

Technical Client Items – on-line vs conventional retail (Gross sales Worth USD)

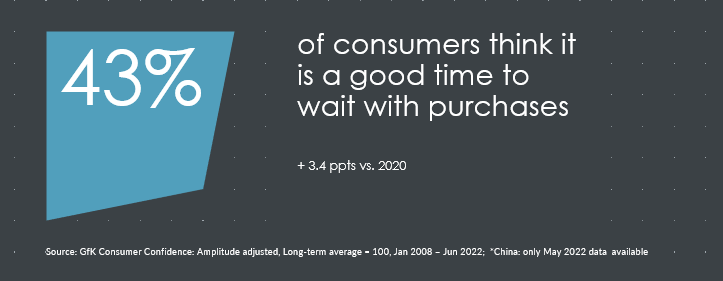

The issue is that this world achieve in share is ready inside a decelerating market of decreasing client spend. As the price of each day residing soars, confidence in private funds is dropping throughout many key age teams. In reality, 43% of individuals globally assume that now’s a greater to delay purchases that to make them (up 3.4 proportion factors in comparison with 2020).

Moreover, the “stickiness” of the brand new on-line procuring habits varies throughout the several types of on-line gamers and markets. For instance, in Europe, the net income of pure gamers (those who solely function on-line) declined by 13% yr so far, whereas click on and mortars (those who function each on-line and on the excessive avenue) declined by 23%. This was anticipated as shoppers regained entry to bodily shops after Covid restrictions lifted globally. Equally, click on and mortar gamers had a relatively greater benchmark for this yr’s development, provided that they skilled greater on-line development that pure gamers, in the course of the pandemic years.

Regionally, the toughest hit has been Western Europe, the place TCG noticed the net gross sales worth fall 4 proportion factors (pp) for year-to-date 2022 in comparison with the identical interval final yr. Subsequent hardest hit has been Japanese Europe and Rising Asia (each down 3 pp), adopted by LATAM (down 2 pp), and Center East & Africa holding comparatively regular (down simply 1 pp). China, the place lockdowns proceed throughout main areas, was one of many few areas to see development in on-line gross sales worth.

Technical Client Items, On-line retail share, Gross sales Worth USD

Namrata Gotarne, World Strategic Insights Director at GfK explains,

“On prime of the general fall in spend as consumers react to the rising price of residing, on-line gross sales have additionally been affected by the lifting of COVID-19 restrictions in most international locations. Sure consumers are reveling of their returned capacity to buy in-store. Regardless that they’re more and more researching on-line for the most effective offers, they’re selecting to purchase instore extra typically in 2022 in comparison with 2021. However we’ve got to think about this as a form of normalization after unprecedented instances for on-line retail; it doesn’t imply that the long-term pattern in the direction of on-line procuring is damaged.”

Retailers’ web sites and social media taking part in an even bigger function in on-line retail

A silver lining is that retailers’ personal web sites are taking part in an even bigger function with consumers than earlier than. This provides retailers a direct voice with these consumers, and the power to ship an omnichannel supply and expertise that brings consumers from their on-line touchpoints into their shops.

Within the first quarter of the yr, 3 out of each 5 consumers globally (61%) went on-line to actively analysis which product to purchase. And, wanting the TCG consumers, 48% (+14 pp in comparison with 2019) of these went onto retailers’ personal web sites to do their analysis. That makes retailer web sites the most well-liked on-line supply utilized by consumers researching merchandise on this class, adopted by search engines like google and yahoo at 42%, after which product assessment websites at 38%.

Social media, too, is taking part in an more and more massive half, creating consciousness and provoking shoppers to buy.

For TCG consumers, 26% (+14 pp in comparison with 2019) went onto social media whereas researching which product to purchase, and 18% confirmed that ads seen on social media impressed them to buy a brand new product. In reality, 15% of shavers had been bought by way of social media platforms in China. In future, digitally native manufacturers will be capable of immediately interact with shoppers by way of social media and never be depending on retailers to drive their gross sales income.

Premiumization on pause as demand drops

Throughout 2020 and 2021, the common worth of TCG gross sales shot up. This was pushed by the massive surge in on-line demand throughout lockdowns, coupled with provide chain challenges, which result in product shortages. This naturally hit merchandise within the decrease and customary worth bands first, forcing shoppers into extra premium choices.

For the reason that finish of 2021, nevertheless, worth rises have been pushed extra by inflationary stress as producers and retailers cross on the rising prices of supplies, core elements, manufacturing and transport. And this has hit the worth of on-line gross sales, as shoppers react to rising prices with a pointy fall in year-on-year demand. In reality, if we examine the common worth of TCG on-line gross sales to that seen in January 2020, we discover that the upward pattern of 2020 and far of 2021 is now flattening, when taken general.

Shoppers are extra worth delicate this yr, retailers are hesitant to extend costs, and producers won’t be able to push via one other spherical of worth will increase with no battle.

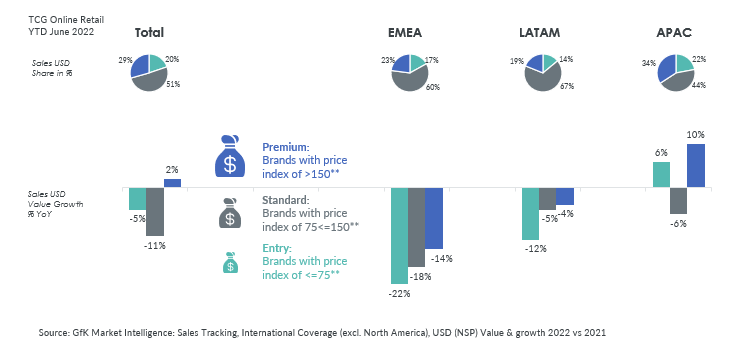

Regardless of this, there are some areas inside on-line retail the place shoppers are nonetheless making rising ranges of purchases within the premium finish. For instance, in APAC, over a 3rd of all TCG gross sales on-line had been premium degree (manufacturers with a worth index of 150 or extra), and returned a ten% improve in worth in comparison with premium gross sales the yr earlier than. For EMEA and LATAM, there was damaging year-on-year development throughout all worth brackets by way of the worth, though premium manufacturers suffered much less severely than customary and entry degree manufacturers.

Premiumization on pause at a broader degree, however seen inside TCG segments

In a panorama of falling demand and tight budgets, manufacturers should put themselves in entrance of shoppers within the channels which can be at the moment being most well-liked by their goal audiences. With retailers’ web sites and social media taking part in an even bigger function within the TCG shopper journey, funding in omni-channel integration and improvement continues to be vital for retailers on this space.

The opposite massive query is worth reductions. Promotions and reductions provided over the primary half of this yr have continued to be at a low degree in comparison with pre-pandemic days. With provide chain disruptions and spiraling prices, producers and retailers alike have aimed toward avoiding reducing into margins. Reductions as much as 10% had been the norm till early this yr, however it will not be a profitable technique for This fall. With the sharp fall seen in demand, and no let-up within the elevated stress on shoppers’ wallets, extra substantial promotions and reductions in This fall will help retailers and types push shoppers to spend a bit greater than deliberate.

![]()