{kind=link}

- There’s a cushion of sizeable unrealized/imbedded good points within the nation’s housing inventory and huge unrealized good points within the US Inventory Market.

- The US has a really robust industrial/company base that has typically improved their stability sheets by rolling over into cheap debt over the past 5 years, and which have maintained excessive revenue margins.

- We’ve got a strong and tight labor market—with stable wage will increase a spotlight of the final a number of years. Importantly within the final 60 years the US has by no means had a recession with no previous spike in preliminary jobless claims.

- The US unemployment price stands at 3.6%—the bottom degree because the begin of the pandemic and solely 0.1% above the 50-year low of February, 2020.

- Some necessary elements of inflation are moderating—the costs of most commodities have fallen significantly over the past 2 1/2 weeks.”

All good factors however let me add a caveat. Issues may be true within the combination however painfully completely different in particular instances. Sure, family financial savings are up, however not for everybody. Half the nation has lower than $400 in financial savings. One-bedroom condo rents are close to $1,500 in lots of locations.

Ditto for companies. The typical firm has a greater stability sheet, however many aren’t common.

Client Shift

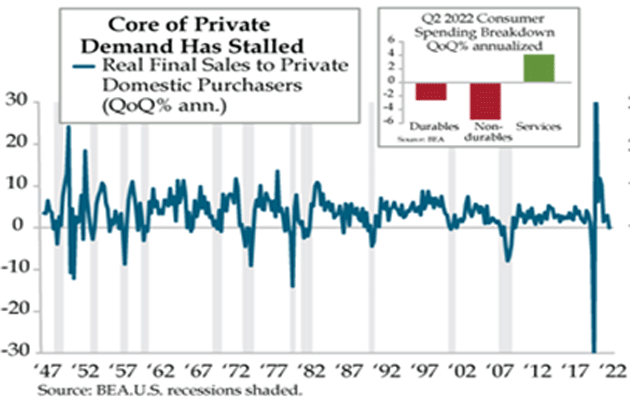

The actual query mark right here is client spending—how a lot it drops and how it drops. We’re within the thick of earnings season and reviews from retailers aren’t good. Walmart (WMT) is extensively watched, not simply by its personal buyers, however as a client well being indicator. Its sheer measurement and nationwide scope reveal rather a lot concerning the financial system.

Walmart’s newest is partly unsurprising: Persons are spending extra on meals and gasoline. The haunting half is that they’re additionally spending much less on issues like attire, furnishings, and different non-essential items. Worse, these occur to be the identical items that had been scarce as a result of provide chain snarls. Now that they’re lastly on the cabinets, folks don’t need (or can’t afford) them. Retailers are overstocked and reducing costs on slow-moving items at the same time as they increase costs on others.

The larger level right here is that client choice is altering… once more. Recall what occurred with COVID: Individuals shifted their discretionary spending from companies to items as a result of the companies have been unavailable or perceived as dangerous.

Now the other is going on. Retailers are lastly getting tailored to new demand patterns simply because the demand goes away. In the meantime airways and trip spots, which had suffered as so many individuals stayed near dwelling, are clogged with extra clients than they will deal with.

Client woes are additionally enterprise woes. Bruce Mehlman summed it up with this from his newest slide deck.

Supply: Bruce Mehlman

All that appears unhealthy, and it’s, however maintain it in perspective. Companies can meet rising prices in a number of methods. The most typical is to chop another type of much less important value or attempt to shift it onto your suppliers. That’s more durable than it was once; many firms have been already working fairly lean after going into COVID survival mode. This from Quill Intelligence:

Supply: Quill Intelligence

Be aware the higher proper field. Shoppers are switching from items to companies.

As for squeezing suppliers… proper now they’re glad simply to have suppliers. I noticed a story from Japan that Toyota is skipping its regular semiannual evaluation and received’t press suppliers for decrease costs. In some instances, it might really pay extra to ensure the important suppliers keep in enterprise.

The opposite alternate options are to lift promoting costs—which may simply backfire when clients are already stretched—or settle for decrease revenue margins. That appears more and more probably for a lot of firms. Coca-Cola, McDonald’s, Proctor & Gamble, and Kimberly-Clark are persevering with to lift costs.

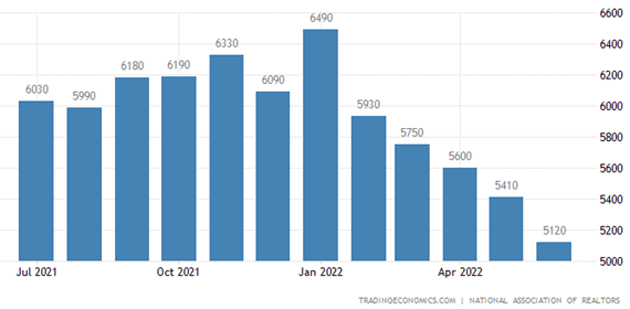

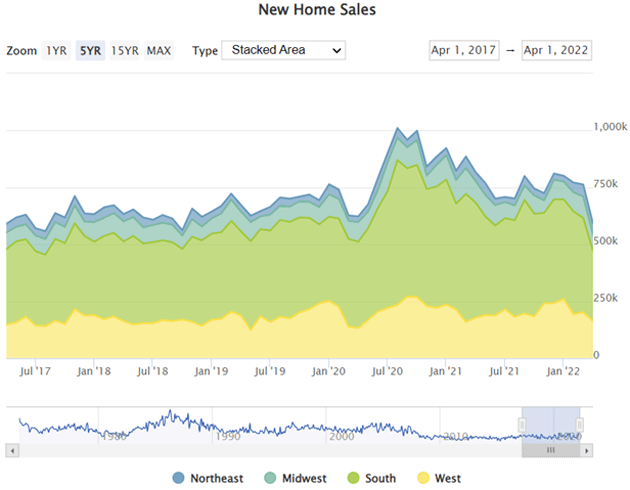

The worst-hit companies might be these most uncovered to larger rates of interest on prime of all the opposite rising costs. Sure, meaning housing. That increase might not flip right into a crash, however it has room to melt fairly a bit, and appears to be within the early phases of doing so. It’s beginning to present in each present and new dwelling gross sales.

Supply: Buying and selling Economics

Supply: Mortgage Information Day by day

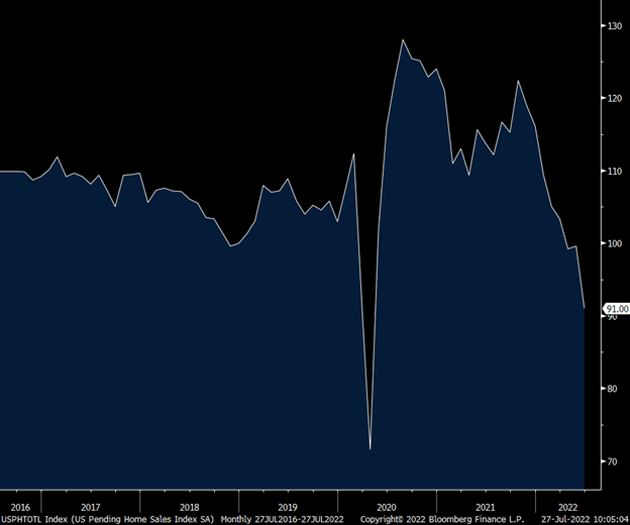

And Pending Residence Gross sales are plunging.

Supply: Peter Boockvar

Be aware that housing drives many different segments like furnishings, paint, home equipment, and so forth. These additionally undergo when dwelling gross sales drop.

All that is in step with a gentle recession situation, which is what we appear to be experiencing up to now. Client spending softer however not an excessive amount of. Unemployment rising however principally in financing-dependent segments like housing and autos. Vitality costs are staying excessive, however folks be taught to handle them. None of that is good however it could possibly be far worse.

Sadly, that not-so-bad near-term outlook collides with some broader forces which are nonetheless coming. It’s probably that the third quarter might be even softer than the earlier two, because the Fed will proceed to lift charges on the subsequent three conferences.

Longer and Deeper

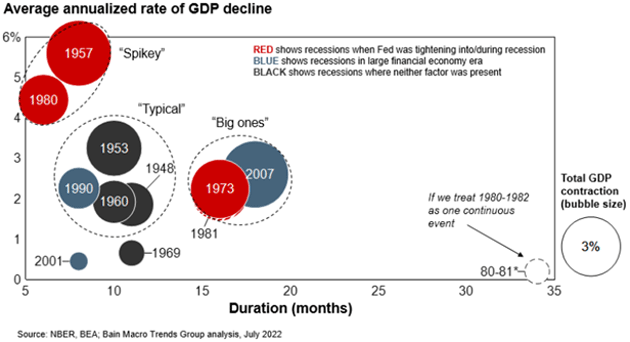

Bain Macro Tendencies Group makes the case that this recession might be most just like the 2007 recession. Right here’s a bit from their longer report.

“As we mentioned within the first piece on this sequence, the present macroeconomic local weather bears a notable similarity to the local weather previous the recession of 2007–2009. That is additionally the one recession in latest historical past that resembles (in depth, length, and tempo) these of earlier high-inflation eras through which the Fed tightened into the contraction (e.g., 1973 and 1981). As Determine 2 illustrates, the recessions of 1973, 1981, and 2007 are a cluster by themselves with respect to length and severity. [Note: The 1981 recession is almost hidden in this cluster graph by the 1973 recession. It’s there.]

“Due to these similarities, we consider firms should take significantly the likelihood that this recession might repeat key components of the recession of 2007–2009.”

Traders are trying on the “dot plots” to see when the Fed may cease tightening and possibly even ease, as that might be a sign to purchase. Possibly sure, possibly no. From David Rosenberg (flagged by Peter Boockvar):

“Bear in mind this: The Fed went on maintain in February 1989, and whereas there was a pleasant tradable rally, the truth is that the low within the fairness market wasn’t turned in till October 1990—twenty months after the pause. The Fed stopped tightening in Might 2000, and the market low didn’t come till October 2002, over two years later. And the Fed moved to the sidelines in June 2006, and the lows didn’t come till March 2009.” I’ll add this, the Fed began reducing charges in January 2001 and the market bottomed in October 2002. The Fed began slashing charges in September 2007 and the market bottomed in March 2009.”

Productiveness Drawback

One ultimate thought. We use GDP as a proxy for financial development. What it actually measures (with a variety of flaws) is output, or manufacturing. That’s the “P” in GDP: Gross Home Product.

On the most simple degree, GDP is just the variety of staff a rustic has occasions the common employee’s output. That’s what we name productiveness. A employee takes one thing—information, constructing supplies, no matter—and provides worth by producing one thing new. Mix all that new worth and also you get GDP development.

In order for you extra GDP, math says you want some mixture of extra staff and/or extra per-worker productiveness. Postwar US financial development occurred for each causes, however primarily productiveness development.

With inhabitants development slowing, GDP has been extra depending on productiveness development. That is changing into an issue. Edward Chancellor defined why within the interview I talked about final week. Right here’s one other half I didn’t quote:

“By aggressively pursuing an inflation goal of two% and always residing in horror of even the mildest type of deflation, they not solely gave us the ultra-low rates of interest with their unintended penalties when it comes to the Every part Bubble. Additionally they facilitated a misallocation of capital of epic proportions, they created an over-financialization of the financial system and an increase in indebtedness. Placing all this collectively, they created and abetted an surroundings of low productiveness development.”

Companies have an curiosity in making their staff as productive as doable. They do that in numerous methods, together with talent coaching and labor-saving expertise. That doesn’t should imply fewer staff. If including robots to your manufacturing unit triples manufacturing with out having to rent extra folks, it additionally triples productiveness. That’s good; it retains costs down and helps extra jobs emerge elsewhere.

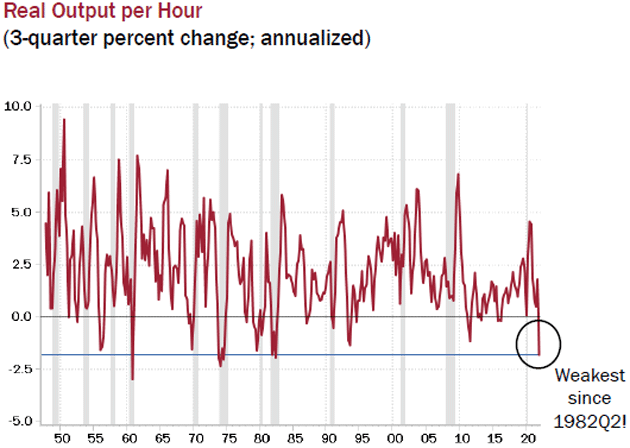

However as Chancellor says, the Fed’s persistently low rates of interest discouraged this course of. We see it within the information. The Bureau of Labor Statistics measures productiveness quarterly. Right here’s the start of their final report on June 2. (The following one is August 9, by the best way.)

Nonfarm enterprise sector labor productiveness decreased 7.3 p.c within the first quarter of 2022, the US Bureau of Labor Statistics reported right this moment, as output decreased 2.3 p.c and hours labored elevated 5.4 p.c. That is the biggest decline in quarterly productiveness because the third quarter of 1947, when the measure decreased 11.7 p.c.

They’re speaking a few quarter when GDP really fell, so it’s no shock output decreased. The shock is that extra work hours produced much less output. That’s not the way it ought to go. And that this was the worst since 1947 ought to concern us.

Right here’s a barely completely different view, once more because of Dave Rosenberg. He illustrates the change in productiveness development on a per-hour foundation. By that measure it’s the worst since 1982.

Supply: Rosenberg Analysis

That’s a loud chart however in the event you take out the final two recession spikes, it appears like productiveness has been broadly declining because the mid-Nineteen Nineties. What might need prompted that?

As they are saying, correlation isn’t essentially causation. However it might be related that that is about when the “Greenspan Put” went from a novel shock to one thing merchants merely anticipated. The 1997 Asian debt disaster and 1998 Lengthy-Time period Capital Administration bailout confirmed we had a brand new type of Fed. So I believe Chancellor is true to pin productiveness declines on the Fed, not less than partially.

Now, add within the demographic components which are shrinking the workforce. And on prime of that, add the not-insignificant variety of pandemic-driven early retirements and “Lengthy COVID” disabilities. Which means we want extra productiveness from the remaining workforce.

That is trying like a problem. United Airways CEO Scott Kirby stated in a latest interview that sickness-related absenteeism is now so excessive, he thinks airways must completely add 4%‒5% extra staff simply to perform the identical quantity of labor. That’s staggering and, if appropriate, I see no cause to suppose it received’t apply in lots of different industries.

If an organization now wants, for instance, 105 staff to supply the identical output that was once doable with 100 staff, it’s unfavourable productiveness development. Not good for earnings and positively not good for GDP.

Might automation assist? In some instances, in all probability so. However between microchip shortages and better financing prices, that’s not getting any simpler. Nor does it remedy each trade’s drawback. McDonald’s CEO Chris Kempczinski talked about automation on the corporate’s final earnings name.

“We’ve spent some huge cash, effort, this. There’s not going to be a silver bullet that goes and addresses this for the trade… The economics don’t pencil out.”

If any restaurant chain might make automation work, it will be McDonald’s. The CEO says it isn’t a silver bullet. Which means his firm—and lots of others—will keep depending on human staff, who’re on common getting much less productive per hour labored.

The place does that lead? Nowhere good. I’ve religion our human ingenuity will discover options, however in the meantime productiveness is a big drawback.

It’s probably going to cap GDP development at a degree none of us will like—which can also be what you’ll anticipate with the huge US debt load. All over the place debt rises (Japan, decide a rustic in Europe, the US), GDP slows. Which is exactly what Lacy Hunt and I and others have been saying for years.

Wanting again on the interval between the 2008 disaster and COVID in 2020, all of us questioned why GDP appeared caught so low. That period’s sluggish development wasn’t a recession, per se, however it was not like previous recoveries.

Now, I’m wondering if we’ll have a equally prolonged interval of even decrease development. After we get by means of this recession, GDP development might gradual to 1%. That might be a recession/restoration like no different in reminiscence.

On the price bizarre issues are taking place, I wouldn’t rule it out.

Cleveland and British Columbia

I’m scheduled to be on the Cleveland Clinic with Dr. Mike Roizen and staff for not less than two days in mid-August. They’ll try my physique doing each impolite factor recognized to man: tubes, scopes, lasers, oh my. COVID delayed my check-up in 2020 so I’m overdue. My physique feels it.

On the finish of August, I get to verify off one in all my bucket listing fantasies and go salmon fishing in British Columbia at a personal camp, reachable solely by helicopter. However the photos look thrilling. I’m trying ahead to 40+-pound Chinook. I’m advised they’re catching nice-sized halibut on the identical fishing holes. I’m not fairly certain of the foundations, however I hope to convey some flash-frozen fish dwelling.

It’s time to hit the ship button. I left extra good materials on the reducing room ground this week than I’ve in a very long time. There’s actually much more to say on this matter. Possibly subsequent time.

Have an ideal week and spend a while with family and friends! And as at all times, don’t overlook to observe me on Twitter!

Your questioning how bizarre this recession will actually be analyst,

John Mauldin