{kind=link}

The mainstream assumption is the established order will proceed on a lot as earlier than. This isn’t simply unlikely, it’s unattainable if whole vitality produced and consumed declines.

Correspondent C.A. submitted this insightful interview with financial strategist and historian Russell Napier: “We Will See the Return of Capital Funding on a Large Scale”.

In Napier’s telling, the 40-year interval from 1980 to 2020 was dominated by central banks (financial coverage) and markets (enterprises searching for to maximise earnings).

These forces fueled the rise of globalization (maximize earnings by arbitraging decrease labor and manufacturing prices abroad through offshoring manufacturing) and financialization (vastly develop debt and leverage however hold debt service low by steadily decreasing rates of interest).

The second-order impact of the ensuing hyper-globalization and hyper-financialization was hyper-dependency on geopolitical rivals and on financial intervention and credit score/asset bubbles to help consumption.

Neither was sustainable. Close to-total dependence on geopolitical rivals in service of private-sector earnings created existential nationwide safety vulnerabilities which should now be addressed by reshoring / homeshoring / friendshoring vital manufacturing.

The market, dominated solely by incentives to maximise earnings by any means accessible, created this vulnerability. It’s incapable of resolving it.

I coated all these dynamics in depth in my guide A (Revolutionary) Grand Technique for the US which predated the Ukraine Battle by 4 months.

Napier sees governments changing central banks as the first pressure in creating credit score and guiding insurance policies / incentives.

He explains that governments don’t need to depend on central banks to create cash or credit score, or on issuing Treasury bonds which might be bought by traders. Governments are guaranteeing business financial institution loans issued by private-sector banks, in impact increasing credit score with out creating extra authorities debt.

These ensures backstop business financial institution loans made in accordance with authorities directives and objectives.

If a borrower defaults, the federal government will cowl the losses so the lender is made entire. It’s riskless lending for banks and retains the increasing credit score off the federal government steadiness sheet.

Napier calls this “the politicization of credit score.”

Napier explains why inflation will probably be maintained in a spread of 4% to six% for years to come back: inflation is the one strategy to cut back the debt burden which has reached $300 trillion globally, and about 250% of GDP of many countries. (That is the entire of each authorities and private-sector debt.)

Napier refers to this as “monetary repression” as a result of inflation that’s greater than bond yields robs savers and advantages debtors, whose earnings rise with inflation whereas their debt service remained fastened. (This assumes fixed-rate loans, in fact.)

This will even restore the buying energy of youthful employees as wages rise, on the expense of older (and wealthier) generations.

The web results of governments taking management of funding and credit score creation “will imply an enormous homeshoring or friendshoring growth, capital funding on a large scale into the reindustrialization of our personal economies.”

Governments must create sufficient credit score to fund each this large capital funding (generally known as CapEx, capital expenditures) and preserve consumption.

Napier factors to the 1946-1979 interval for instance of governments guiding the economic system greater than central banks guiding the economic system.

All this makes wonderful sense, however Napier overlooks three consequential dynamics:

1. The vitality cliff, as hydrocarbon manufacturing declines sooner than new sources will be introduced on line to exchange them.

2. The demographic cliff as workforces decline and the cohort of retirees to be supported balloons.

3. The impossibility of funding large new CapEx and infrastructure spending, supporting the ballooning cohort of retirees and client spending to maintain the “waste is progress / Landfill Financial system” buzzing whereas preserving inflation tamed to five%.

In different phrases, there will probably be tradeoffs. If you’d like reasonable inflation (politically crucial, as excessive inflation loses elections) and big will increase in CapEx, client spending has to take a success.

Moreover, inflation will probably be pushed by two forces: scarcities of necessities like meals and vitality, that are mainly the identical factor in industrialized fertilizer-dependent agriculture, and the growth of credit score in extra of will increase in productiveness.

If $1 invested in CapEx generates extra worth by way of items and companies, meaning productiveness is rising. If CapEx doesn’t generate extra items and companies, productiveness is stagnant.

As I’ve defined, that is what occurred within the Seventies: large CapEx was invested in retooling the U.S. industrial base to cut back air pollution and enhance effectivity.

The discount in air pollution significantly improved well-being however didn’t improve GDP or productiveness. We solely handle what we measure, and since we don’t measure well-being, the true positive factors of this CapEx weren’t even measured.

Like well-being, we don’t measure Nationwide Safety economically, so enhancements within the safety of our manufacturing of necessities is not going to even be acknowledged.

The true positive factors of homeshoring received’t even be acknowledged or understood except we throw out the present methodology of financial measurements and exchange it with a modernized set of measurements that aren’t restricted to manufacturing and consumption (i.e. “progress”.).

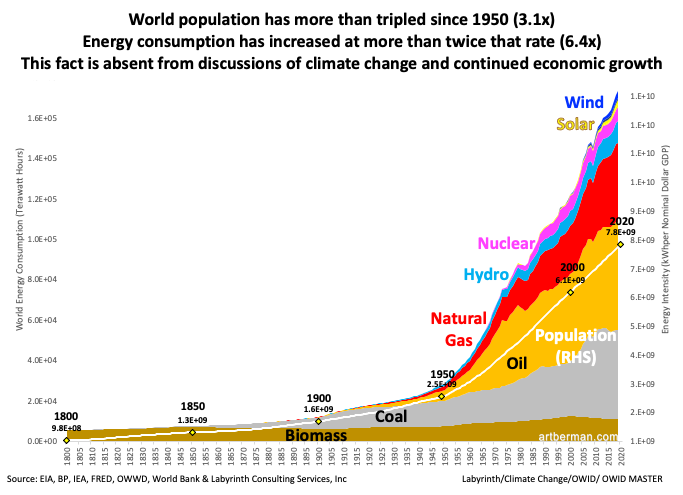

As for vitality, what most individuals miss is Jevon’s Paradox: including sustainable vitality (nevertheless you outline that) doesn’t exchange our consumption of hydrocarbons, it merely will increase our whole consumption of vitality.

One other issue most individuals miss is the dimensions of the hydrocarbon advanced everyone seems to be hoping to exchange, and the timeline of that alternative.

Regardless of many years of funding, different vitality provides solely 5% or so of world vitality. These pounding the desk for nuclear vitality hardly ever point out the timeline for setting up sufficient vegetation at scale to make a distinction: many years, not years.

Because the cheap-to-get oil has been extracted, what’s left prices extra. Sure, know-how improves, however physics wins in the long run; extra vitality should be expended to get the hard-to-get oil out of the bottom.

These realities dictate an Power Cliff during which oil manufacturing declines sooner than new sources will be introduced on-line. And reasonably than eat extra vitality as new sources are introduced on-line, we’ll eat much less and it’ll price extra, for all the explanations I defined in my guide.

The demographic cliff is equally baked in. The workforce of the following decade can’t be expanded, it’s already right here, together with the hovering cohort of retirees.

If sacrifices should be made in consumption attributable to greater prices of necessities and the necessity for enormous CapEx, the buyer economic system will shrink.

Because the system is optimized for growth, that contraction will upend the whole world economic system as it’s at the moment configured.

On high of those three elements, there’s the hovering healthcare prices generated by life-style illnesses (diabesity, and many others.), excessive ranges of air pollution in growing nations and the getting older populace.

Profiteering doesn’t generate well being, and profiteering has been the secret so lengthy few can think about another way of life.

The mainstream assumption is the established order will proceed on a lot as earlier than. This isn’t simply unlikely, it’s unattainable if whole vitality produced and consumed declines.

As vitality analyst Vaclav Smil put it: “I’m not an optimist or a pessimist. I’m a scientist.” Slightly than waste time arguing about optimism and pessimism, let’s deal with physics, prices and timelines, i.e. sensible assessments, and on the trade-offs wanted to achieve our aim of a sustainable, open-to-all, truthful economic system.

This essay was first printed as a weekly Musings Report despatched solely to subscribers and patrons on the $5/month ($50/12 months) and better degree. Thanks, patrons and subscribers, for supporting my work and free web site.