{kind=link}

The large debt ranges present the one most important threat and problem to the Federal Reserve. It’s also why the Fed is determined to return inflation to low ranges, even when it means weaker financial development. Such was some extent beforehand made by Jerome Powell:

“We have to act now, forthrightly, strongly as we’ve been doing. It is vitally necessary that inflation expectations stay anchored. What we hope to attain is a interval of development beneath pattern.”

That final sentence is a very powerful.

There are some necessary monetary implications to below-trend financial development. As we mentioned in “The Coming Reversion To The Imply Of Financial Development:”

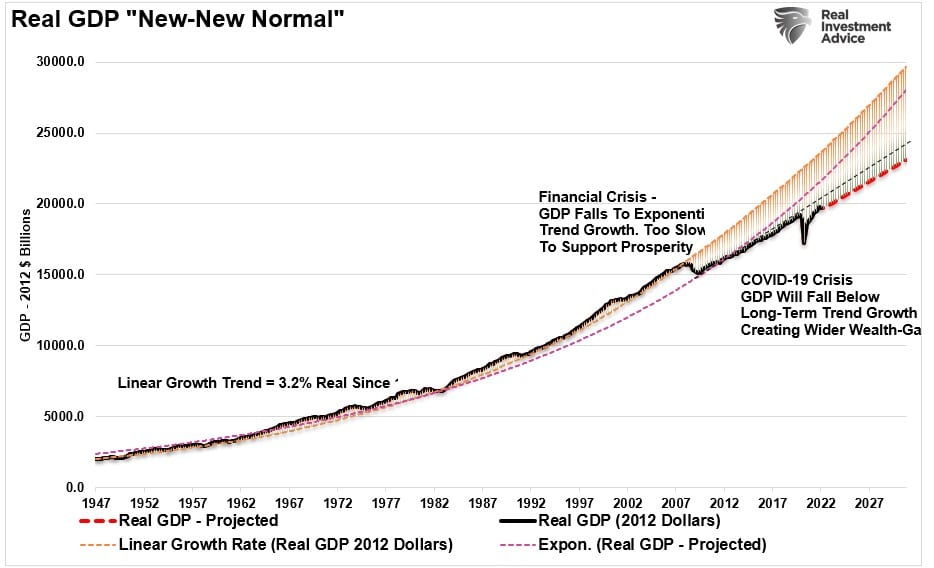

“After the ‘Monetary Disaster,’ the media buzzword grew to become the ‘New Regular’ for what the post-crisis economic system would really like. It was a interval of slower financial development, weaker wages, and a decade of financial interventions to maintain the economic system from slipping again right into a recession.

Put up the ‘Covid Disaster,’ we’ll start to debate the ‘New New Regular’ of continued stagnant wage development, a weaker economic system, and an ever-widening wealth hole. Social unrest is a direct byproduct of this “New New Regular,” as injustices between the wealthy and poor change into more and more evident.

If we’re right in assuming that PCE will revert to the imply as stimulus fades from the economic system, then the ‘New New Regular’ of financial development can be a brand new decrease pattern that fails to create widespread prosperity.”

As proven, financial development tendencies are already falling in need of each earlier long-term development tendencies. The Fed is now speaking about slowing financial exercise additional in its inflation battle.

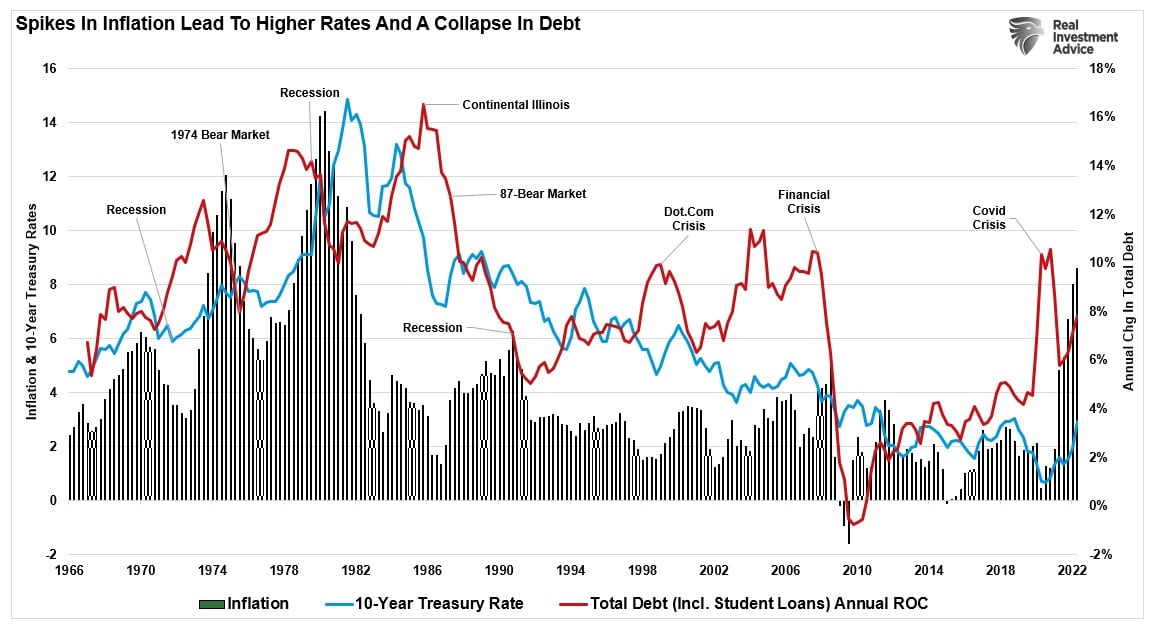

The explanation that slowing financial development, and killing inflation, is essential for the Fed is as a result of huge quantity of leverage within the economic system. If inflation stays excessive, rates of interest will alter, triggering a debt disaster as servicing necessities enhance and defaults rise. Traditionally, such occasions led to a recession at greatest and a monetary disaster at worst.

The issue for the Fed is attempting to “keep away from” a recession whereas attempting to kill inflation.

Recessions Are An Vital Half Of The Cycle

Recessions will not be a nasty factor. They’re a essential a part of the financial cycle and arguably an important one. Recessions take away the “excesses” constructed up in the course of the growth and “reset” the desk for the following leg of financial development. With out “recessions,” the build-up of excesses continues till one thing breaks.

Within the present cycle, the Fed’s interventions and upkeep of low charges for greater than a decade have allowed basically weak corporations to remain in enterprise by taking over low cost debt for unproductive functions like inventory buybacks and dividends. Customers have used low charges to increase consumption by taking over debt. The Authorities elevated money owed and deficits to document ranges.

The belief is that elevated debt is just not problematic so long as rates of interest stay low. However therein lies the lure.

The Fed’s mentality of fixed development, with no tolerance for recession, has allowed this example to inflate reasonably than permitting the pure order of the economic system to carry out its Darwinian perform of “hunting down the weak.”

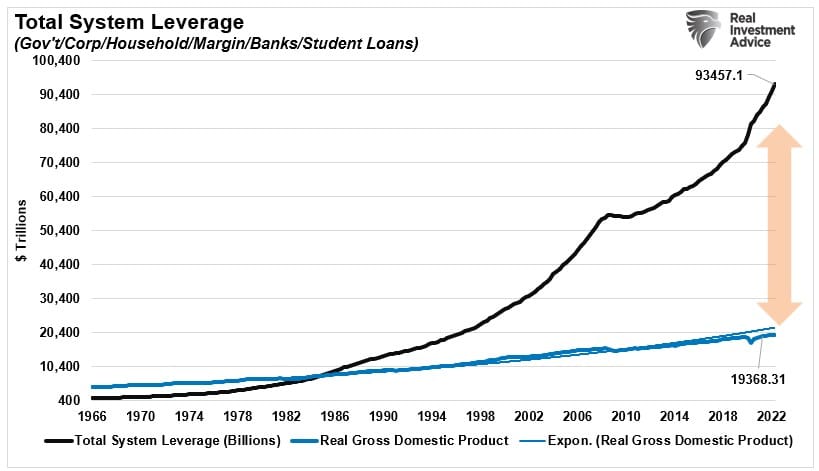

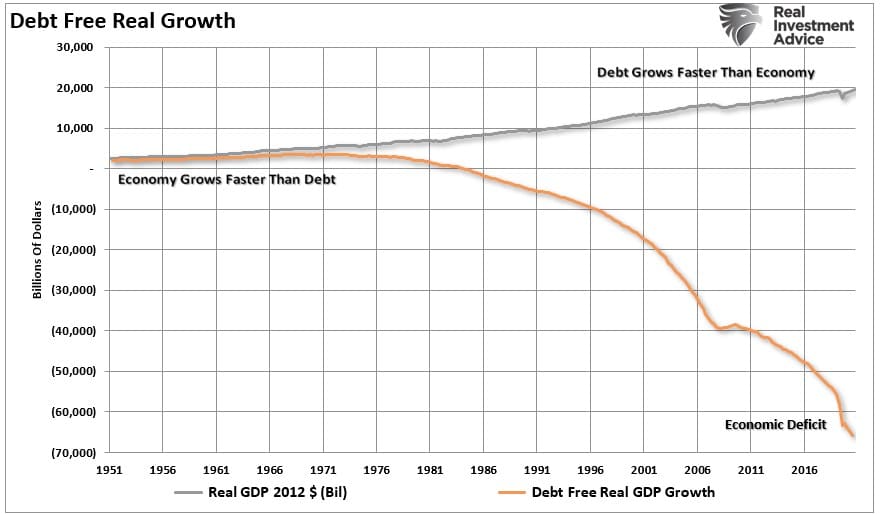

The chart beneath reveals whole financial system leverage versus GDP. It presently requires $4.82 of debt for every greenback of inflation-adjusted financial development.

Extra Debt Doesn’t Resolve Issues

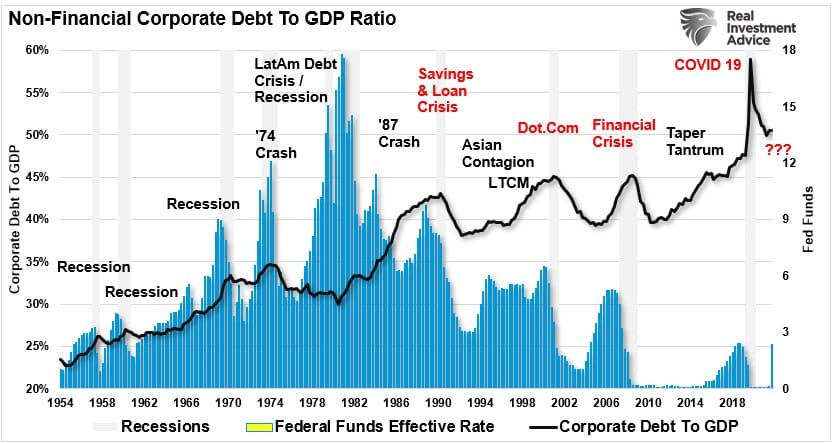

Over the previous few many years, the system has not been allowed to reset. That has led to a resultant enhance in debt to the purpose that it impaired the economic system’s development. It’s greater than a coincidence that the Fed’s “not-so-invisible hand” has left fingerprints on earlier monetary unravellings. On condition that credit-related occasions are likely to manifest from company debt, we will see the proof beneath.

Given the years of “ultra-accommodative” insurance policies following the monetary disaster, a lot of the capability to “pull-forward” consumption seems to have run its course. Such is a matter that may’t, and gained’t be, mounted by merely issuing extra debt. After all, for the final 40 years, such has been the popular treatment of every Administration. In actuality, a lot of the combination development within the economic system was financed by deficit spending, credit score creation, and a discount in financial savings.

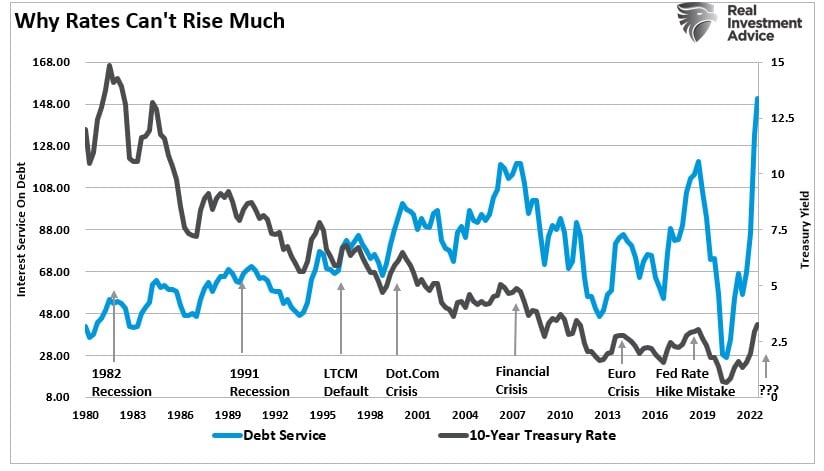

In flip, this surge in debt diminished each productive investments and the output from the economic system. Because the economic system slowed and wages fell, the buyer took on extra leverage, reducing the financial savings fee. Consequently, will increase in charges divert extra of their disposable incomes to service the debt.

A Lengthy Historical past Of Horrible Outcomes

After 4 many years of surging debt towards falling inflation and rates of interest, the Fed now faces its most troublesome place for the reason that late 70s.

The U.S. economic system is extra closely levered immediately than at another level in human historical past. Since 1980, debt ranges have continued to extend to fill the earnings hole. Larger homes, televisions, computer systems, and so forth., all required cheaper debt to finance them.

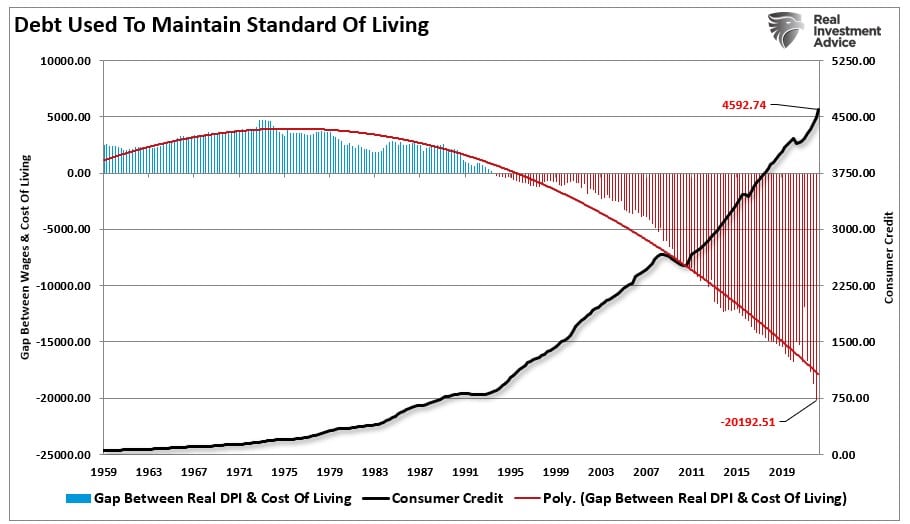

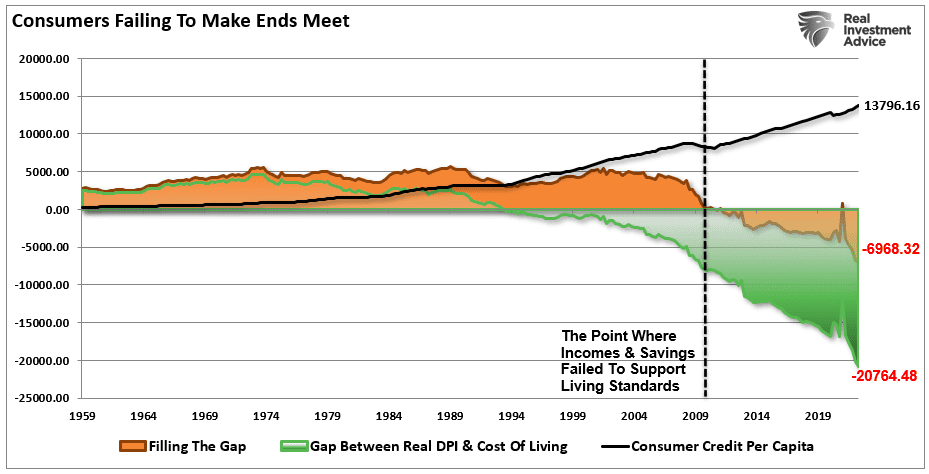

The chart beneath reveals the inflation-adjusted median dwelling commonplace and the distinction between actual disposable incomes (DPI) and the required debt to assist it. Starting in 1990, the hole between DPI and the price of dwelling went unfavorable, resulting in a surge in debt utilization. In 2009, DPI alone might not assist dwelling requirements with out utilizing debt. As we speak, it requires virtually $7000 a 12 months in debt to take care of the present lifestyle.

The rise and fall of inventory costs have little to do with the typical American and their participation within the home economic system. Rates of interest are a wholly totally different matter. Since rates of interest have an effect on “funds,” will increase in charges shortly negatively influence consumption, housing, and funding, which in the end deters financial development.

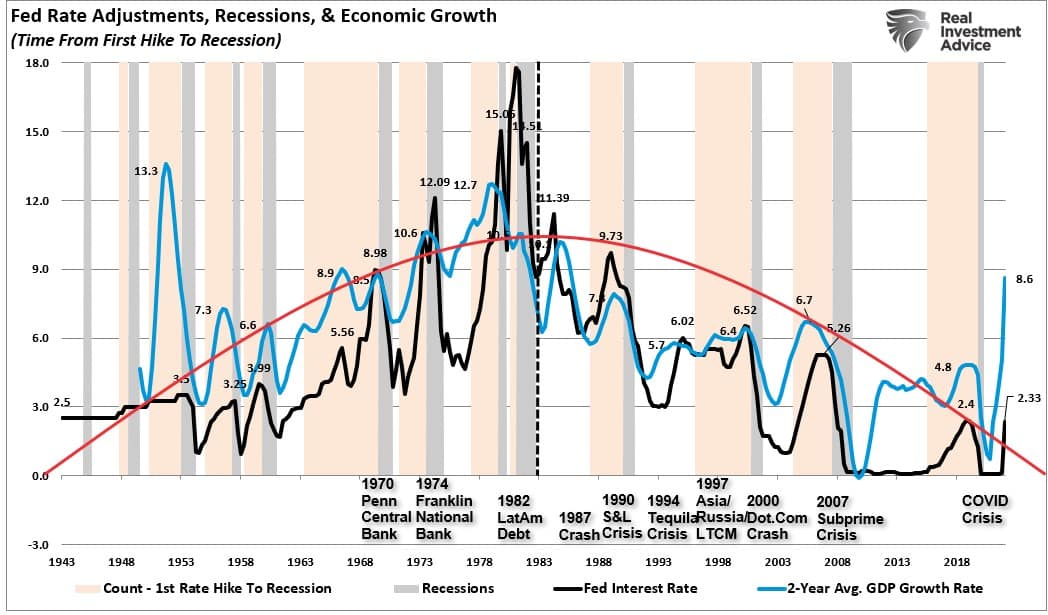

Since 1980, each time the Fed tightened financial coverage by mountaineering charges, inflation remained “nicely contained.” The chart beneath reveals the Fed funds fee in comparison with the buyer value index (CPI) as a proxy for inflation. The present bout of inflation is fully totally different, and because the Fed hikes rates of interest to gradual financial demand, it’s extremely possible they are going to over-tighten. Historical past is replete with earlier failed makes an attempt that created financial shocks.

The Fed’s Problem

The Fed has a tricky problem forward of them with only a few choices. Whereas growing rates of interest could not “initially” influence asset costs or the economic system, it’s a far totally different story to recommend that they gained’t. There have been completely ZERO instances in historical past the Federal Reserve started an interest-rate mountaineering marketing campaign that didn’t ultimately result in a unfavorable consequence.

The Fed is now starting to cut back lodging at exactly the mistaken time.

- Rising financial ambiguities within the U.S. and overseas: peak autos, peak housing, peak GDP.

- Extreme valuations that exceed earnings development expectations.

- The failure of fiscal coverage to ‘trickle down.’

- Geopolitical dangers

- Declining yield curves amid slowing financial development.

- Report ranges of personal and public debt.

- Exceptionally low junk bond yields

Such are the important components required for the subsequent “monetary occasion.”

When will that be? We don’t know.

We all know that the Fed will make a “coverage mistake” as “this time is totally different.”

Sadly, the end result possible gained’t be.